SOURCE ITEMS

The dour tone of the report was reinforced by declines among discretionary items such as automobiles, furniture and electronics. Demand at grocery stores, service stations and general merchandise retailers also declined.

…

The labor market continues to provide the wherewithal for Americans to spend. Payrolls bounced back in April with a 223,000 increase following a 85,000 gain the prior month, and the jobless rate fell to 5.4 percent, the lowest since May 2008, according to Labor Department data.

U.S. Retail Sales Disappoint Again, BloombergBusiness, May 13, 2015. Accessed May 13, 2015.

—————

Published by the Federal Reserve Bank of St. Louis. Accessed May 13, 2015.

—————

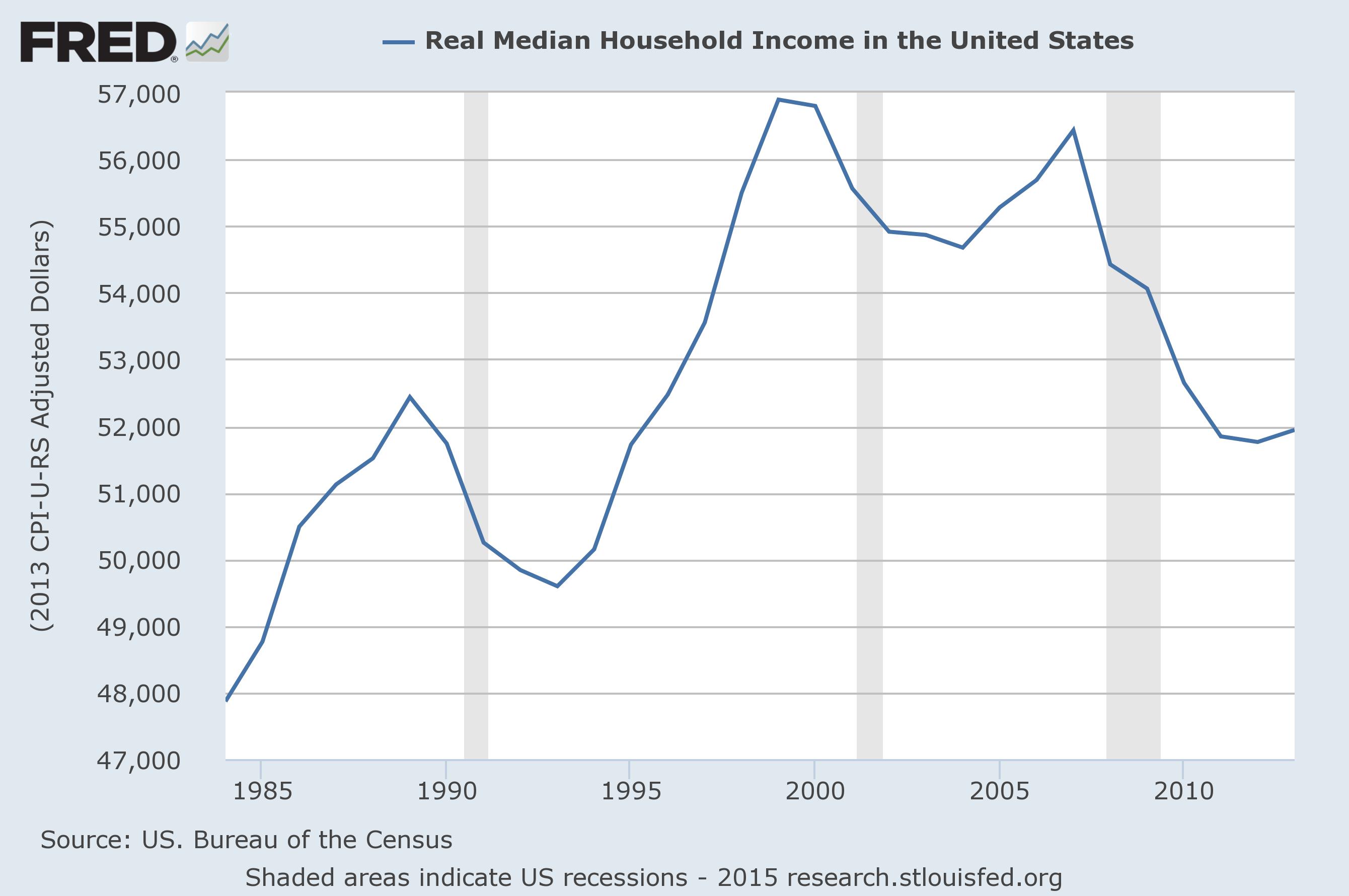

The Sentier Research monthly median household income data series is now available for March. The nominal median household income was down $307 month-over-month but up $1,104 year-over-year. That’s a -0.6% MoM decline and a 2.1% YoY increase.

Doug Short, Median Household Income Declined in March, Advisor Perspectives, April 23, 2015. Accessed May 13, 2015.

COMMENTS

Economists and journalists seem to have lost the ability to connect the dots. Repeatedly, they report the numbers but fail to talk about how they are connected in the real world.

Very few of us are isolated consumers. We are members of families and households, so household income is a much more meaningful indicator of ability to increase spending. In families and households we talk about what to buy and often share incomes, even if only through informal borrowing from each other.

Household income is a function of total hours worked by members of the household and wage levels. Thus, even if the take home pay of a member of a household is rising, if other members are working fewer hours or not at all, then household income can actually decline.

Unemployment is not the only source of declining work hours for a household. Withdrawing from the labor force is another way that household income can decline substantially, even while the wages of those who are formally counted in the labor force continue to rise. For a very long time, the labor force participation rate in the U.S. has been falling. With every tick downward, the number of earning hours for households ticks downward. This takes its toll on household income and ability to spend.

When we think about the people who withdraw from the labor force, the retirement of baby boomers readily comes to mind. What tends not to come to mind is the number of middle and lower income households in which young people are neither working nor looking for work and the number of two-earner households in which one of the earners is working part-time or sporadically or taking a personal sabbatical until the chances of landing a job get better.

Slowly rising wages can do very little to lift consumer spending while labor force participation continues to decline.